In 2021, self storage was the darling of the Wall Street Journal, with the paper declaring the industry “The Pandemic’s Hot Property.” Last week, the same outlet reported that self storage rents and occupancy had fallen to record lows as the “Pandemic Boom Cools.” But is this really accurate?

The reasons for the decline stem from the aftermath of the pandemic. Corporate spaces and fitness centers have largely reopened, eliminating a lot of the need for home offices and gyms and freeing up space in people’s homes. In addition, rising mortgage rates have led to fewer home sales, reducing the kind of moves that often necessitate temporary or permanent storage.

So while there is no denying a slow down, the media has largely ignored key nuances in their reporting, raising the eyebrows – and the ire – of many in the industry. So what was it that the WSJ overlooked in its rush to declare such a precipitous drop in demand?

The New Self Storage Normal

“Rental rates and demand have declined from the heights of 2020-21, but that was to be expected,” says Chris Sonne, Executive Vice President, Newmark Valuation & Advisory Group. “What we’re seeing is the classic ‘reversion to the mean.’ There was a huge spike due to Covid, and things are just returning to normal.”

Sonne adds that despite this, the ‘new normal’ is still running high for the industry. “Normal for self storage, according to the National Association of Real Estate Investment Trusts (NAREIT), has been a 16+% annual return for more than 25 years. That’s better than apartments, industrial and office facilities, etc.,” explains Sonne. “Through boom and bust cycles, and even the great financial crisis, self storage performs. The article’s forecast of a potential demise is greatly exaggerated.”

Cory Sylvester, Co-Founder of DXD Capital and Radius+, a data intelligence company focused on the self-storage industry, felt similarly. He was interviewed for the WSJ piece, and told the outlet, “Some of the more abnormal demand patterns have just come back to normal levels.”

Unfortunately, Sylvester’s more positive take was buried within the overall negative tone of the story. He took to Linkedin to state he felt the story was "pretty negative," so MSM followed up with him for more information.

Sylvester told us that comparing the performance of self storage now to the days of Covid is unfair. While the Journal focused on facilities cutting rents by record levels (“At some locations, rents for new customers are as much as 28% below what they were in the summer of 2021”), he says looking at rates through the lens of the pandemic will of course paint a different picture versus comparing pre- and post-Covid rates.

“What they should have focused on,” Sylvester explains, “was that rental rates have merely stabilized, not fallen dramatically.”

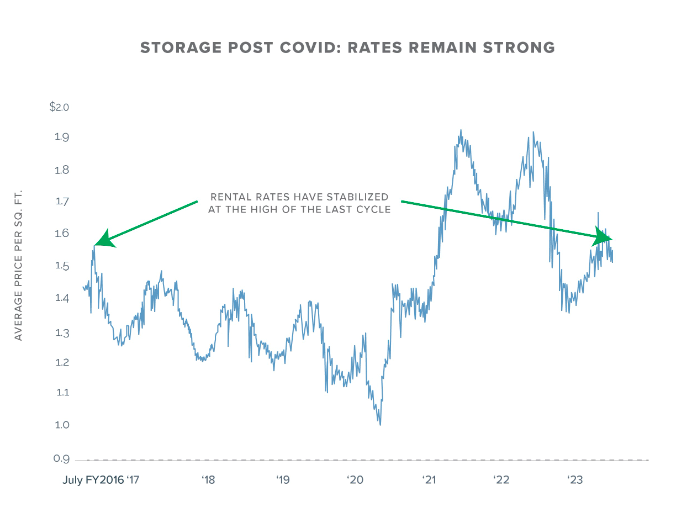

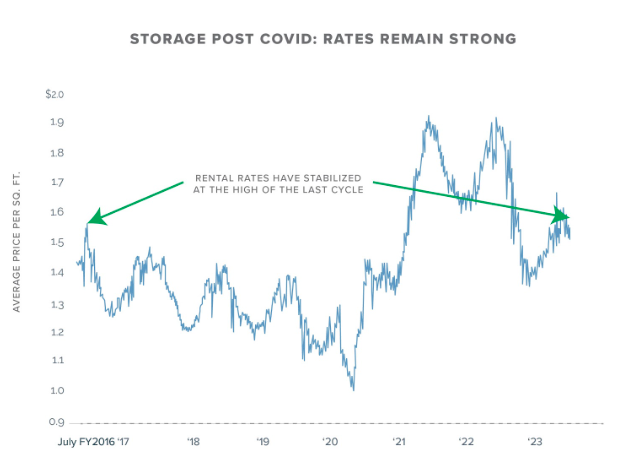

Sylvester gave MSM permission to republish the following chart, which he first presented in his own newsletter. “This highlights what the WSJ’s report missed,” says Sylvester. “While the industry may be down 20% from 2021, it is still at the highs of 2016.”

Source: DXD Capital, Radius+

Source: DXD Capital, Radius+

“Furthermore,” he adds, “I would expect this to be the bottom and for rates to grow from here starting in 2024.”

The Rent Price Fallacy

To support its assertions that self storage is in a slump, the report also trumpeted how several facilities, including Public Storage, are giving away units for $1 for the first month. In defense, Sylvester says this is a common practice. “Offering the first month free or for $1 is just an incentive, it’s nothing new.”

Sylvester says assumptions about the industry based on spot rates such as these are not a true indicator of industry health. “On the surface, just using rental rates may show a downturn,” he says. “But pricing structures have changed.”

To provide further insight, he offers the following: “In the past, a facility may have offered a 10×10 for $140, and then raised the rent in 9-12 months. Now, to get people in the door, they’re offering that same unit for $120, but then aggressively raising the rate after six months to make up the difference.”

“Without perspective, it’s easy to see how it looks like self storage is losing. Spot rates indicate that,” acknowledges Sylvester. “But that’s the front-end of the rent curve pulling things down, without looking at the back-end. So it looks like a decline, when in reality, it’s not. It’s just a restructuring of pricing. Rents are still growing above inflation.”

Investors Remain Secure

The WSJ said it – so shouldn’t stocks be plummeting? “We haven’t seen any market reaction due to the article, no one is pulling out of deals, no equity money is drying up for the sector,” confirms Sonne.

While the WSJ asserts that “the NAREIT Equity Self Storage index has fallen more than 20% since the end of 2021,” Sonne counterpoints. “This is a short-term view of things. Since 2002, REITs are up 1200%. That’s a 13% compound rate annually, and that’s just the pricing.”

He says the numbers look even better when analyzing single asset pricing. “20 years ago, the price per square foot for a rental was just under $60 nationwide. In 2022, it’s more than $160. That’s an annual compound rate increase of more than 5.10%. These are good numbers, whether boom or bust. You can’t argue with that.”

While investors should always keep an eye on the market, cause for concern is also exaggerated. Sonne says, “At the peak in 2020, stocks were up over 70%. They’ve since corrected, yet are still up over 10% YTD. So, if you bought stock prior to the pandemic, you’re still up 60%.”

“Being the Wall Street Journal, I’m surprised they didn’t mention that,” laughs Sonne.

The WSJ did highlight recent deal activity among some of the sector’s biggest firms in its wrap-up. Sonne says it should not have been an afterthought. “Self storage has had the largest year in sector history, with more than $15 billion in portfolio transactions in 2023. The investment community has greatly expressed its confidence in the sector.”

“Either the Wall Street Journal or $15 billion is right,” says Sonne. “I think it’s the latter.”

—

THIS JUST IN: Further evidence of a healthy self storage outlook arrived today, with the release of Public Storage’s second quarter financial results. According to the press release, the REIT witnessed record customer move-in volume growth of 13.6%, stabilized same store NOI growth of 6.6%, and non-same store lease-up NOI growth of 20%.

“These factors led to an increase in our outlook for the back half of the year,” said Joe Russell, President and Chief Executive Officer of Public Storage.

—

Brad Hadfield is a staff writer and news researcher for Modern Storage Media. He also manages the MSM website.

Popular Posts

Joe Shoen is taking a stand. In our...

Self-storage software is no longer...

Joe Shoen has had enough.

The self storage industry is in a precarious...

From policy pivots in Ottawa to tariff...

Joe Shoen, CEO of U-Haul, has had enough.

In a record-breaking deal finalized May 12,...

This interview is from July 24, 2024.

Rising tides lift all ships, but in 2025 it...

Some recent lower court decisions have been...

Recent Posts

As self-storage demand continues to grow in...

When customers entrust their physical...

The self-storage industry has spent the...

The self-storage industry has spent the...

For two decades, Andrew Hess’ job was...

Uniti, a provider of AI-powered agents for...

The shift toward automation in self-storage...

We live in the future now. Everything’s...